By using our website, you agree to the use of cookies as described in our Cookie Policy

Ready to apply for business funding?

Start our simple online application now.

![]()

![]()

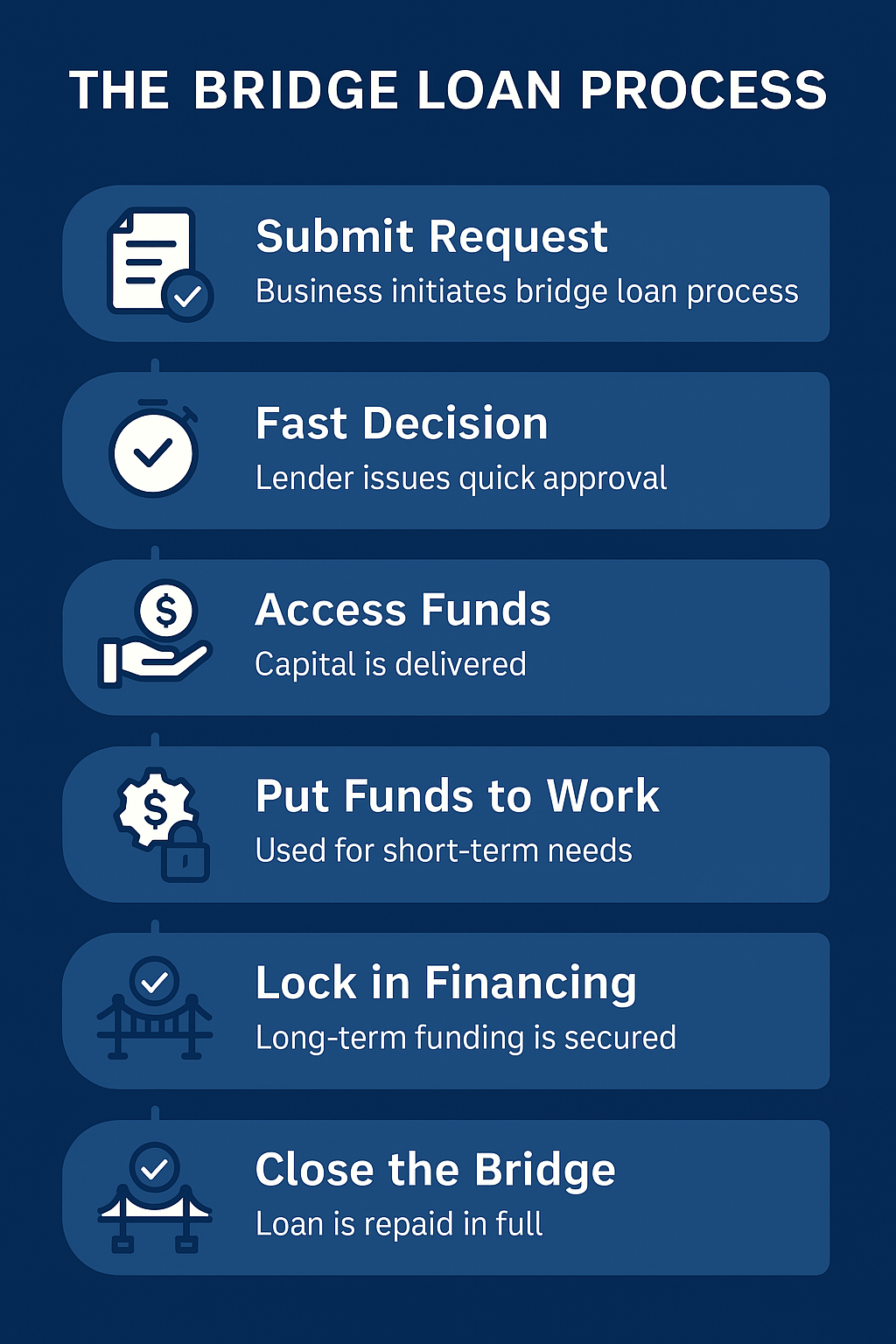

When timing is tight and a long-term loan isn't moving fast enough, a bridge loan can provide the short-term solution your business needs. Whether you're waiting for another loan to close or need to jump on an opportunity before permanent financing is in place, bridge loans fill the gap.

Think of it like putting up support beams to hold your roof while you fix the walls - it gives you the stability you need until everything's properly in place.

A bridge loan is a short-term loan designed to provide immediate capital while a business secures more permanent financing. It acts as a temporary solution that "bridges the gap" between current needs and future funding. Typically lasting from a few months to a year, it allows business owners to move quickly when time-sensitive opportunities arise.

According to the National Association of Realtors, nearly 20% of commercial real estate deals involve some form of short-term financing to close before long-term funds become available.

Bridge loans aren’t designed to replace long-term loans. They’re meant to help you avoid missing out while the rest of your financing catches up.

They can be a smart move for growing businesses that have a clear strategy in place but need to act quickly. The key is knowing how to use them, when to pay them off, and what the exit plan looks like. Without that clarity, short-term debt can become long-term trouble.

Bridge loans function like a quick injection of cash, usually backed by some form of collateral. They're often interest-only loans with balloon payments due at the end of the term, which is why timing and repayment planning are so important.

Think of it like putting down a deposit to hold a property before the mortgage paperwork clears. Fast, focused, and not meant to last forever.

These loans cost more than traditional financing, but they help you act quickly when opportunities arise. Think of it as paying a bit extra for express shipping. Sometimes the speed is worth the premium.

Let’s say your business is acquiring a second location. You've found the perfect space, but your SBA loan won’t close for another 90 days. Rather than risk losing the property, a bridge loan provides the funding you need now so you can lock in the deal and finalize permanent financing later.

Bridge loans are not meant to be cheap. Rates are typically higher than standard loans, and you’ll often need to provide some form of security to qualify. But for businesses with predictable incoming funding, the speed can be worth the premium.

One common misconception is that a bridge loan is just a fast loan anyone can get. In reality, they require solid collateral and a clear repayment plan. Lenders are betting on your ability to close the long-term deal.

Bridge loans aren't the right fit for every business. If your monthly income fluctuates significantly or you're not confident about your upcoming revenue, these loans can add financial stress. For example, if you run a seasonal business with long quiet periods, the regular payment schedule might be tough to maintain.

Similarly, if you're counting on future funding that isn't guaranteed, like a pending contract or an investment deal that's still in talks - it's smart to hold off. The quick repayment timeline means you need steady, reliable cash flow to stay on track.

Think of it like choosing between a sprint and a marathon - short-term loans are fast and intense, while longer-term options give you more breathing room but take longer to set up.

Used correctly, a bridge loan keeps things moving while you finalize the bigger picture. It’s a tool, not a crutch.

Approval timelines are usually much faster than traditional loans. Lenders will look closely at your collateral, repayment plan, and existing financing in progress.

Most lenders want to see that your business has both a near-term need and a concrete exit strategy.

Expect shorter applications, faster underwriting, and more emphasis on deal timing than detailed financials.

Some lenders may approve you within days if everything is lined up.

While both offer flexibility, a business line of credit is typically best for covering recurring short-term expenses such as payroll or inventory. It works more like a credit card where you draw, repay, and reuse (see: Understanding Business Lines of Credit). However, credit limits are often much lower, and if you need a lump sum quickly, a bridge loan is far more efficient. Bridge loans are ideal for larger, time-sensitive needs that exceed what a revolving line of credit can support.

Term loans offer fixed repayment schedules and lower interest rates, making them a better fit for long-term investments or planned growth, but they often require more documentation, underwriting, and time to close. If you’re racing against the clock - whether it’s securing a property or acquiring a business, bridge loans offer the speed and simplicity that term loans can’t match, even if they cost more in the short run.

Merchant cash advances are known for lightning-fast funding, often within 24 hours, but that speed comes with high fees and daily repayment terms tied to revenue. This can put pressure on your cash flow, especially in slower months. Bridge loans are usually more structured and predictable, making them a safer option when you need a large sum without draining daily operations.

Hard money loans are commonly used in real estate, secured by property value rather than creditworthiness. They tend to have even higher interest rates and fees than bridge loans and are often backed by private investors. Bridge loans, on the other hand, are typically offered through institutional or business lenders and come with more standard terms. If you’re not in a real estate-specific funding deal, a bridge loan is usually more practical and less volatile.

Invoice factoring lets you sell outstanding invoices for immediate cash, ideal for businesses with large accounts receivable. However, it doesn’t work if you’re funding an expansion, covering a deposit, or making a capital purchase. Bridge loans are more flexible in how they’re used and aren’t tied to your invoicing volume, making them a better fit for non-receivables-based needs.

When you’re purchasing a specific piece of equipment, equipment loans are hard to beat. They’re asset-backed, offer favorable terms, and are purpose-built. But if your funding needs go beyond one asset, like covering down payments, renovations, or holding costs while waiting for equipment loans to close - a bridge loan offers broader use and quicker access.

SBA loans are often the most affordable and reliable form of long-term business funding. The downside? They take time - weeks or even months to secure. Bridge loans give you the ability to act now and close on urgent deals while the SBA process plays out in the background. Many business owners use both, starting with a bridge loan and rolling it into an SBA loan once approved.

Personal loans like those offered by SoFi, LightStream and others, are easier to apply for and can offer quick funding, but they’re not designed for business use. Limits are lower, interest rates can be higher, and you’re personally liable for repayment regardless of how your business performs. Bridge loans are structured specifically for business transactions, often with better scale, use-case alignment, and repayment terms specific to the funding lifecycle.

If your business needs to act fast and has a reliable path to permanent financing, a bridge loan can be a smart tool. Just don’t treat it as a substitute for long-term funding.

Use it to close the gap, not create a bigger one.

If you check both boxes, it’s worth having a conversation, but remember, you should:

The more clarity you have, the better decisions you’ll be able to make.

Need fast capital to bridge a funding gap? BusinessCapital.com makes it easy to apply for bridge loans online in minutes.

Apply here or call 877-400-0297 to speak with a funding advisor today.

See How Much Capital Your Business Can Access & Start Growing Today!

Apply Now

Sign up for our newsletter to get exclusive updates and offers

Start our simple online application now.

See what our clients have to say about their experience with us.

![]()

© 2025 BusinessCapital, LLC

![]()