By using our website, you agree to the use of cookies as described in our Cookie Policy

Ready to apply for business funding?

Start our simple online application now.

![]()

![]()

Big money changes everything. A $5 million line of credit isn't just another loan—it's a financial tool that completely changes how your business works. Unlike regular loans that make you take all the money at once, a credit line lets you grab cash exactly when you need it.

You only pay for what you use, when you use it.

For successful businesses with solid sales, this kind of financing is a game-changer. Whether you're looking to expand into new markets, buy important equipment, buy out a competitor, or just want a safety net for surprise opportunities, a $5 million credit line puts serious financial power in your hands.

Let's look at what sets apart businesses that can get this kind of financing from those that can't—from what you need to qualify and what paperwork you'll need to how to make the most of it once you have it.

A business line of credit works like a financial safety net, not a one-time cash dump. Unlike a term loan that forces you to take the whole amount upfront, a credit line lets you pick and choose—you take exactly what you need while leaving the rest untouched and interest-free.

At the $5 million level, you're playing with the big boys. This isn't just extra cash for day-to-day stuff; it's money that can transform what your business can do. Think of it like a super-powered business credit card—it works the same way but with much higher limits and better terms, perfect for making big business moves.

The best part? It's revolving—as you pay back what you've used, that money becomes available again without having to apply for a new loan. This creates a permanent money source that grows with your business.

Many business owners find this revolving setup becomes essential during growth. You rarely need all your money at once—you might need $1 million for new equipment in January, another $800,000 for inventory in March, and $1.2 million for a property in June. A credit line handles this natural business rhythm without making you apply for multiple loans or pay interest on money sitting idle.

As your business gets bigger, having access to serious cash becomes less of a luxury and more of a necessity. A $5 million business line of credit lets you do things that smaller loans simply can't handle.

Having access to this much money lets you make major growth moves:

You can buy out competitors when you have enough cash to move quickly. You can expand into new regions or markets instead of just talking about it. You can launch major new products or services with proper funding instead of cutting corners. You can build new facilities or open new locations on your timeline, not when the bank finally approves your loan.

In these situations, timing is everything. Businesses with quick access to cash get better deals and move faster, while competitors get stuck waiting for financing. Your credit line becomes more than just money—it becomes a strategic advantage that lets you make confident decisions backed by real cash.

For established businesses with big operations, having access to this much credit keeps everything running without hiccups:

You can buy inventory in bulk to get better prices. You can handle cash flow during seasonal ups and downs without stress. You can make payroll during expansion without worry. You can handle clients who take 90 days to pay without it hurting your business. You can fill working capital gaps without disrupting operations.

Day-to-day operations for bigger businesses create unique money challenges, even when you're profitable. When you land a major client who pays on 90-day terms, you might face three months of production costs before seeing a dime. Having a big credit line gives you the breathing room to handle these timing mismatches without giving up growth opportunities.

Having access to cash makes your business more resilient when things get tough:

You can survive market downturns with enough financial cushion. You can respond to industry changes proactively instead of reactively. You can handle emergencies or critical repairs without shutting down. You can pay unexpected tax bills or meet new regulations quickly. You can work around supply chain problems by finding alternative suppliers or stocking up.

Business survival depends directly on financial flexibility. When unexpected challenges hit, businesses with cash access adapt quickly while competitors struggle with limited options. This might mean switching to new suppliers during shortages, fixing critical equipment immediately, or staying open during industry downturns while less-prepared competitors close shop.

Here's how businesses could use these credit lines:

A manufacturing business could use $2 million to install automation that boosts production by 40% while cutting labor costs. A growing retail chain could use $3.5 million to open three new locations at once, speeding up their market growth. A tech company could use $1.8 million to buy a competitor with valuable technology, strengthening their market position. A construction company could draw $4 million to fund a major project while waiting for progress payments, letting them take on bigger jobs than their competitors.

These examples show how flexible cash access creates real business results. The manufacturer doesn't just buy equipment—they transform how efficiently they can produce. The retailer shrinks their expansion timeline from years to months. The tech company buys innovation instead of building it from scratch. The construction company takes on projects they couldn't touch before.

Getting approved for a $5 million business line of credit means meeting tougher standards than for smaller loans. According to a recent Federal Reserve Small Business Credit Survey, only about 40% of businesses receive the full amount of financing they request. Lenders need solid proof that your business has the financial strength to handle this level of credit.

Lenders look for established businesses with a proven track record:

You typically need 2-3 years in business minimum, with 5+ years getting you better terms. Your revenue should show steady growth or stable performance in your market. You need to show profit across multiple years. Your business model needs to be proven in the real world. Your credit history should show you've handled other loans responsibly.

Your past performance is the best predictor of future reliability. Businesses that have weathered multiple business cycles while staying profitable show resilience that makes lenders confident. Similarly, if you've managed smaller credit lines responsibly, you build credibility for larger amounts. This is why established businesses typically get better terms than newer ones, even if they have similar current finances.

Your business needs to show enough revenue to support a loan of this size:

You typically need $5-10 million in annual revenue minimum. Your monthly revenue should consistently hit $400,000-$800,000. Your profit margins need to match or beat industry standards. Your revenue should come from multiple clients, not just one or two big ones. Your cash flow needs to be predictable based on past performance.

Revenue requirements reflect a simple reality: paying back a $5 million credit line requires generating substantial cash. Lenders typically expect your monthly revenue to be much higher than your potential monthly payments. They pay special attention to revenue diversity—if 80% of your income comes from a single client, that's risky. Businesses with multiple revenue streams, predictable seasonal patterns, and strong margins look much better to lenders.

Both your business and personal credit scores matter for approval:

Your business credit score typically needs to be 650+ minimum, with higher scores getting better terms. Your personal credit score generally needs to be 680+ minimum. Your credit history should be free from recent bankruptcies or defaults. Your business should have established credit profiles with major credit bureaus. Your payment history should show consistency across all your bills.

Credit scores provide a standardized way to assess risk based on how you've paid bills in the past. For big credit lines, both business and personal scores factor into the decision because lenders see financial responsibility as a complete picture. Many business owners are surprised that personal credit affects business financing, but lenders see it as an important clue about how you'll handle business obligations. Building strong business credit through vendor relationships, smaller credit lines, and consistent payments creates the foundation for accessing bigger financing.

Credit lines this big typically require substantial assets to back them up:

Business assets like equipment, inventory, and real estate often serve as primary collateral. Accounts receivable (money clients owe you) provide additional security. Personal guarantees from business owners are standard requirements. Commercial property or owned facilities may be used. Investment accounts or other liquid assets can strengthen your application.

Collateral requirements directly reduce lender risk by providing security against the credit they extend. While some smaller credit lines might be unsecured, at the $5 million level, substantial collateral typically becomes necessary. Specific requirements vary by industry—manufacturing businesses might use equipment and inventory, while service businesses might rely more heavily on accounts receivable and personal guarantees. Lenders generally prefer collateral that holds its value and could be sold relatively easily if needed.

Good documentation significantly improves your chances of approval. For a $5 million business line of credit, you need thorough financial paperwork that proves your business can handle this level of financing.

Prepare these financial documents with careful attention to detail:

Balance sheets covering 2-3 years show your assets and liabilities. Profit and loss statements (both monthly and annual) show your revenue patterns. Cash flow statements showing your history help prove you can manage money. Current accounts receivable and payable reports reveal your collection and payment practices. Year-to-date financial statements show your current performance.

Financial records tell your business's story through numbers. Lenders analyze these documents to understand your revenue patterns, expense management, profit trends, and overall financial health. Missing information or inconsistencies raise red flags, while complete, professional documentation builds confidence. Many businesses work with their accountants to prepare "lender-ready" financial packages that present information in formats lenders prefer, making the review process smoother.

Tax documents verify your financial reporting:

Business tax returns for 2-3 years show filing consistency. Personal tax returns for all owners (2-3 years) show income flow. Tax extension documentation explains any filing delays. Business tax ID verification confirms legal standing. Sales tax returns demonstrate compliance where applicable.

Tax documents serve as independent verification of the financial information you provide. Lenders compare your financial statements with your tax filings to ensure consistency. Big discrepancies can derail your application, so your accountant should be ready to explain any differences between tax returns and financial statements. For pass-through entities like S-corporations and LLCs, personal tax returns show how business income flows to owners, providing additional context for lender evaluation.

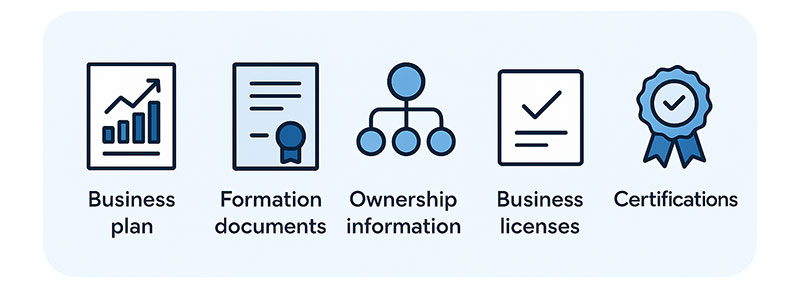

Lenders need to understand your business structure and operations:

Business plans with detailed projections show your strategic direction. Formation documents (articles of incorporation, etc.) clarify your legal structure. Ownership information and organizational charts show who controls what. Business licenses and permits verify regulatory compliance. Industry-specific certifications validate specialized qualifications.

These documents help lenders understand your business beyond the numbers. Your business plan shows strategic thinking and provides context for how the credit line fits into your growth plans. Formation documents and ownership information clarify legal structure and responsibility. Licenses, permits, and certifications verify that you're operating legitimately within your industry and have the necessary qualifications. Together, these elements build a complete picture of your business for lenders to evaluate.

For assets backing your credit line:

Recent professional appraisals of business property or assets establish current values. Equipment lists with values and serial numbers document tangible assets. Real estate deeds or ownership documentation confirm property ownership. Vehicle titles and valuations catalog transportation assets. Inventory lists with current market values quantify product assets.

Collateral documentation establishes both the value and ownership of assets backing your credit line. Recent, professional appraisals carry much more weight than owner estimates, particularly for high-value items like real estate or specialized equipment. Detailed inventory and equipment lists should include purchase dates, current values, and identifying information. For accounts receivable used as collateral, aging reports and customer information help lenders assess collectability. The more organized and detailed these records, the more value lenders assign to your collateral.

Getting a $5 million business line of credit involves a straightforward process that most lenders follow with some variations.

The process starts by understanding what you really need:

You'll have a focused discussion about your business and funding needs. The lender will give you an honest assessment of your qualification chances. They'll clearly explain your options and terms. You'll get answers to your specific questions. You'll learn what documentation you need to prepare.

This initial conversation helps both you and the lender determine if there's a good fit before investing significant time in the application process. Be prepared to discuss your business model, revenue, and specific funding needs. Honest communication about your financial situation saves time and helps the lender guide you toward the most appropriate options. This is also your opportunity to ask questions about terms, timelines, and requirements so you can make an informed decision about proceeding.

Prepare and submit your formal application:

You'll complete the lender's application form with business details. You'll gather and submit all required documentation. You'll provide authorization for credit checks and background verification. You'll answer any follow-up questions promptly. You'll sign necessary disclosures and agreements.

See How Much Capital Your Business Can Access & Start Growing Today!

Apply Now

The formal application process requires attention to detail and complete documentation. Missing or incomplete information is the most common cause of delays, so take time to ensure everything is accurate and thorough. According to SBA research on small business financing, applications with complete documentation are processed up to 30% faster than those requiring follow-up. Working with your accountant or financial advisor to prepare a complete package can significantly improve both your chances of approval and the speed of processing.

The lender evaluates your application thoroughly:

They'll verify all financial information you've provided. They'll analyze your business performance and projections. They'll assess collateral values and ownership. They'll review your credit history and scores. They'll evaluate industry risks and market conditions.

Underwriting is the most detailed part of the process, where lenders thoroughly evaluate your business's ability to handle the credit line. This typically takes 2-4 weeks for large credit lines, though it can be faster with well-prepared documentation. During this time, the lender may request additional information or clarification on specific points. Staying responsive to these requests keeps the process moving. The underwriter's job is to assess risk from multiple angles – financial performance, credit history, collateral value, industry outlook, and management capability all factor into the decision.

If approved, you'll review and accept the offer:

You'll receive formal approval with detailed terms. You'll review interest rates, fees, and repayment requirements. You'll understand any covenants or restrictions. You'll negotiate any terms that need adjustment. You'll accept the offer by signing the agreement.

The approval stage is when you'll see exactly what the lender is offering. Take time to thoroughly understand all terms and conditions before accepting. Pay particular attention to interest rates (including how they're calculated and whether they're fixed or variable), fees (both upfront and ongoing), repayment requirements, and any covenants that might restrict certain business activities. If some terms don't work for your situation, this is your opportunity to negotiate. Once you sign the agreement, you're legally bound to its terms, so make sure they align with your business needs and capabilities.

Once approved, you'll gain access to your credit line:

The lender will set up your account and access methods. You'll learn how to draw funds when needed. You'll understand reporting requirements and account management. You'll receive contact information for ongoing support. You'll get access to online account management tools.

After approval, the final stage is setting up your access to the credit line. Most lenders provide multiple ways to draw funds, including online transfers, dedicated checks, or direct payment to vendors. You'll also learn about any reporting requirements, such as periodic financial statements or inventory reports. Understanding how to effectively manage your account from the beginning helps you maximize the benefits of your credit line while maintaining a positive relationship with your lender. Many lenders assign a relationship manager for credit lines of this size who serves as your primary contact for questions or future needs.

Want to increase your chances of getting approved for a $5 million business line of credit? These strategies can help strengthen your application.

Check both business and personal credit reports for errors. Pay down existing debt to improve your debt-to-income ratio. Resolve any outstanding tax liens or judgments. Make all payments on time for at least 12 months. Establish trade lines with suppliers who report to credit bureaus.

Credit improvement takes time, so start this process well before applying for a major credit line. Errors on credit reports are surprisingly common – according to the Federal Trade Commission, about 20% of consumers have errors on their credit reports that might affect their scores. Disputing these errors can provide a quick boost to your scores. Reducing your overall debt utilization (the percentage of available credit you're using) can also significantly improve your scores, even if you can't pay off all debts. For business credit, establishing relationships with vendors who report to business credit bureaus helps build a stronger profile that lenders can evaluate.

Improve your cash position before applying:

Tighten up collection processes to reduce outstanding receivables. Build cash reserves to demonstrate financial stability. Document how you handle seasonal fluctuations successfully. Highlight recurring revenue streams that provide predictable income. Show how you adjust expenses based on revenue patterns.

Cash flow management directly impacts your ability to service debt, making it a critical factor in credit line approvals. Improving your collection processes and reducing outstanding receivables strengthens your cash position. If your business experiences seasonal fluctuations, document how you successfully manage these cycles. Recurring revenue streams like subscriptions or service contracts are particularly valuable as they demonstrate predictable future income. Expense management matters too – showing that you can adjust spending based on revenue fluctuations demonstrates financial discipline that lenders value.

A strong business plan shows how you'll use and repay the credit line:

Include detailed projections showing return on investment. Explain exactly how you'll use the credit line. Include market analysis backing up your growth plans. Outline how you'll handle risks. Show off your industry expertise and competitive advantages.

Your business plan connects the dots between getting financing and achieving business success. For a $5 million credit line, lenders want to see thoughtful planning about how the funds will generate returns that support repayment. Specific use cases with projected outcomes carry more weight than general statements about growth. Market analysis demonstrates that you understand your competitive landscape and have identified realistic opportunities. Risk assessment shows that you've considered potential challenges and have contingency plans. Together, these elements present a compelling case that the credit line is not just affordable but a strategic asset for your business.

Once you've secured your $5 million business line of credit, using it strategically makes all the difference. Smart management ensures this financial tool helps your business thrive instead of becoming a burden.

Use your credit line wisely for maximum benefit:

Only pull funds for planned, strategic purposes. Avoid using the credit line for routine operating expenses. Try to keep utilization below 50% when possible. Track each draw and its specific business purpose. Monitor the return on investment for funds used.

Strategic fund usage maximizes the value of your credit line while minimizing costs. Reserve your credit line for investments and opportunities that generate returns exceeding your borrowing costs. Using a $5 million credit line for everyday expenses can create dependency and reduce available capital when major opportunities arise. Many businesses maintain a utilization target of 30-50%, ensuring they have capacity for unexpected needs while demonstrating responsible usage to lenders. Tracking the purpose and outcomes of each draw helps evaluate which uses deliver the best returns and informs future decisions about credit line usage.

Smart repayment keeps your credit line healthy:

Pay on time or early to build payment history. Pay more than the minimum when cash flow allows. Set up automatic payments to avoid late fees. Pay off higher-interest portions first. Keep clear records of all payments and balances.

Repayment strategy affects both your current finances and future borrowing options. Consistent, on-time payments build positive credit history that can lead to increased limits or better terms in the future. Paying more than the minimum when possible reduces interest costs and maintains available credit for new opportunities. Some credit lines have different rates for different types of draws – prioritizing repayment of higher-interest balances maximizes your savings. Automatic payments eliminate the risk of missed due dates and associated penalties, which can be substantial on large credit lines.

Keep close tabs on your credit line status:

Review account statements as soon as they arrive. Track utilization rates and available credit. Monitor interest rates and fees. Match credit line transactions with your accounting system. Regularly review how the credit line is supporting your business goals.

Active account management prevents surprises and ensures your credit line remains aligned with business needs. Regular statement reviews help catch any errors or unexpected charges quickly. Tracking utilization rates helps maintain appropriate balances and avoid approaching limits that might trigger higher rates or concerns from lenders. Integrating credit line activity with your accounting system provides a complete financial picture and simplifies tax preparation. Periodic reviews of how the credit line supports your business goals help ensure this powerful financial tool continues to serve your strategic objectives rather than becoming just another expense.

Maximize the strategic value of your credit line:

Fund opportunities with clear ROI. Use the credit line to negotiate better supplier terms. Time major purchases to align with business cycles. Outmaneuver competitors with your financial flexibility. Build a history of responsible use to qualify for higher limits.

Strategic credit line usage creates competitive advantages that extend beyond simple access to capital. Having funds readily available allows you to negotiate better terms with suppliers, such as discounts for early or upfront payments that exceed your borrowing costs. Timing major purchases to align with your business cycles optimizes cash flow and reduces carrying costs. The ability to move quickly on opportunities while competitors are arranging financing can secure better deals and faster implementation. Consistently demonstrating responsible management of your credit line builds a track record that supports future financing needs as your business continues to grow.

A $5 million business line of credit isn't just financing—it's rocket fuel for your business ambitions. With this level of capital at your fingertips, you can seize major opportunities, navigate challenges with confidence, and accelerate your growth trajectory while competitors struggle to keep pace.

At BusinessCapital.com, we've helped thousands of businesses secure the funding they need to reach new heights. With over $5 billion funded to U.S. businesses and an A+ BBB rating, we understand what it takes to qualify for substantial financing and how to structure it for maximum benefit.

Don't let limited capital hold your business back. Take the next step toward financial power and flexibility today.

Call 877-400-0297 to speak directly with a funding advisor about your specific situation, or apply online in minutes for a same-day decision.

Sign up for our newsletter to get exclusive updates and offers

Start our simple online application now.

See what our clients have to say about their experience with us.

![]()

© 2025 BusinessCapital, LLC

![]()