By using our website, you agree to the use of cookies as described in our Cookie Policy

Ready to apply for business funding?

Start our simple online application now.

![]()

![]()

Access to capital can determine whether a business grows or stalls. The way you borrow is just as important as the amount you borrow. Business lines of credit and business loans are two of the most common financing tools, but they serve very different purposes. Choosing the wrong structure can lead to cash flow strain, inefficient debt, and lost momentum.

Here’s how to evaluate both options with clarity.

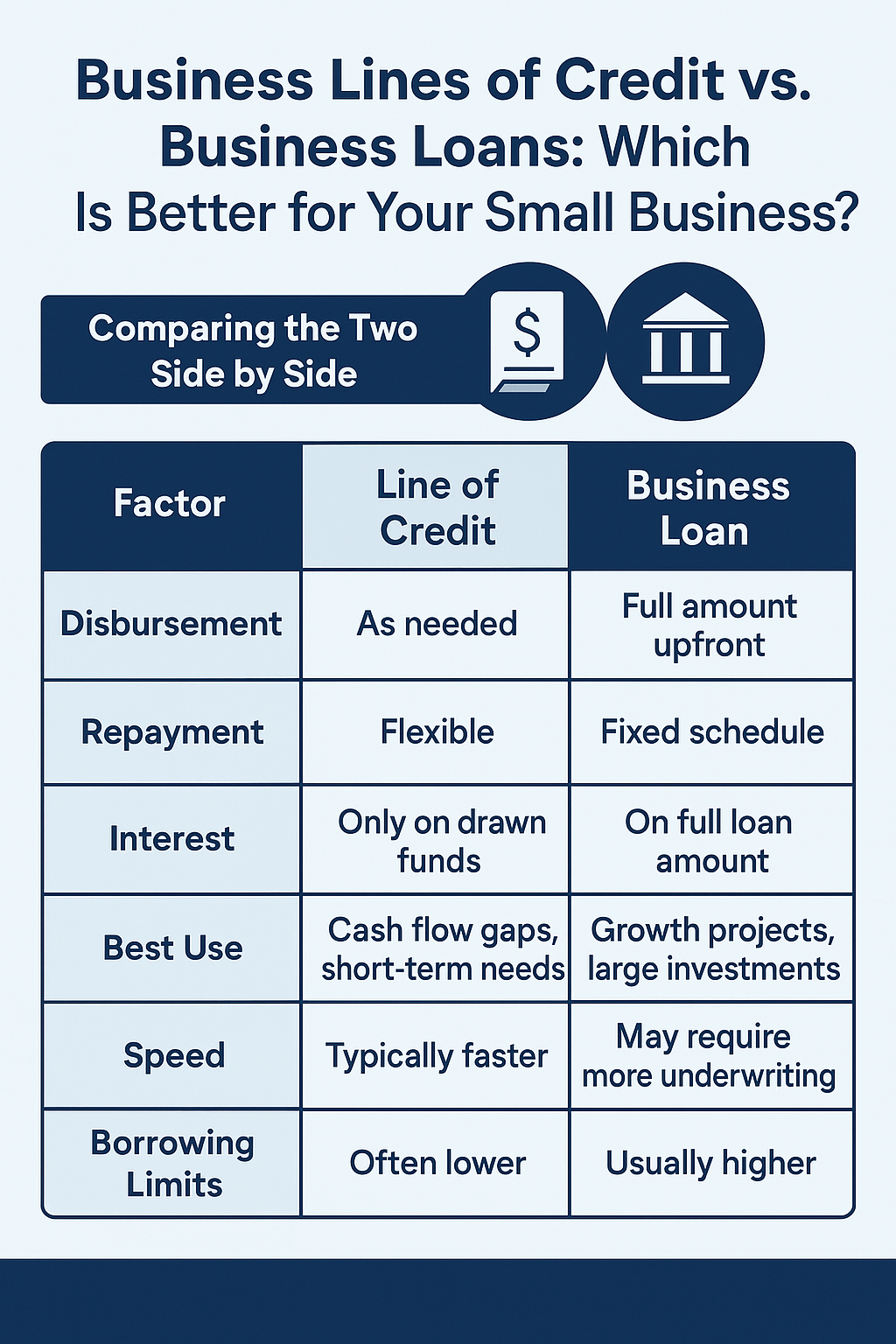

A business line of credit gives you access to a pre-approved amount of funding that you can draw from when needed. You’re not required to take the full amount upfront. Instead, you borrow only what you need when you need it and repay it on your own schedule. Interest is only charged on the amount you draw.

This setup provides flexibility, making it easier to manage fluctuations in revenue or unexpected expenses.

If your business experiences highs and lows throughout the year, or if your capital needs are inconsistent, a line of credit helps you stay prepared without overextending. It’s essentially a buffer, ready when you need it, without the pressure of using it all at once.

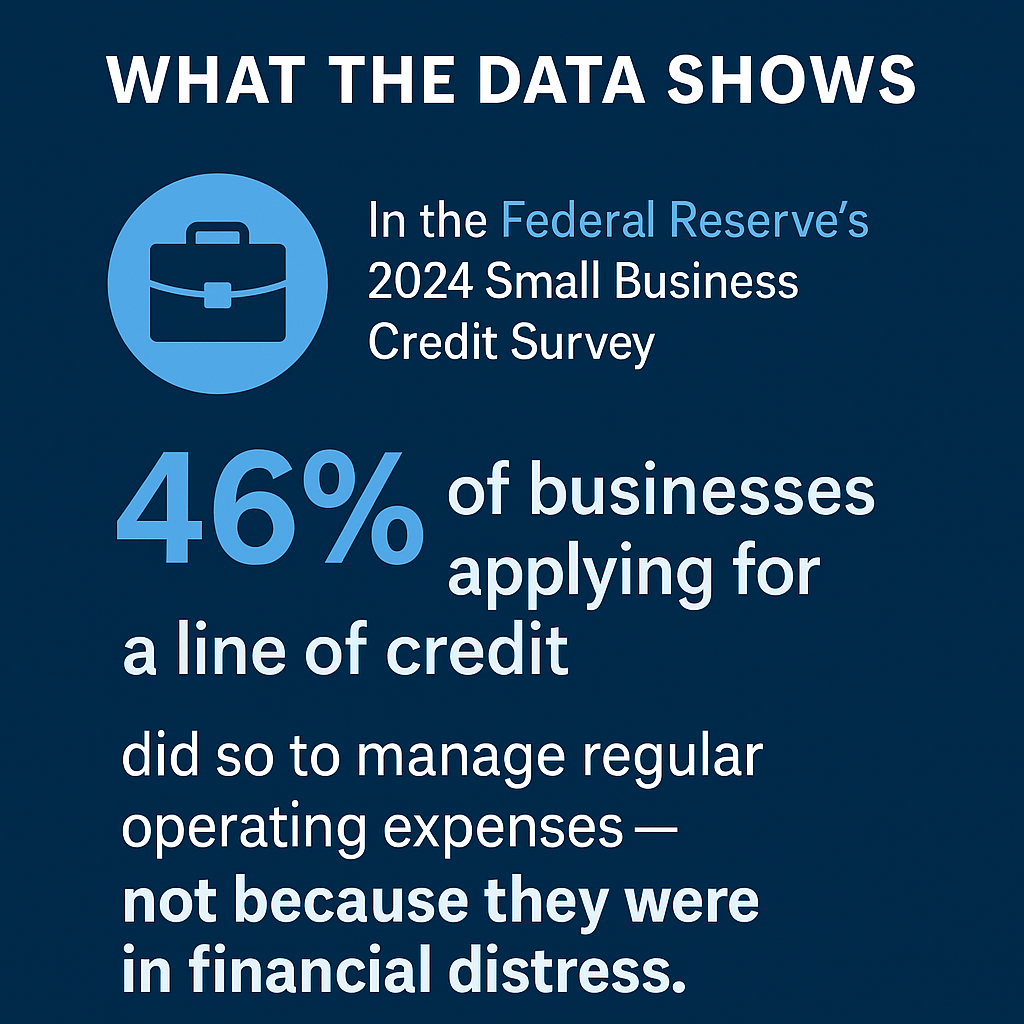

Lines of credit are often misunderstood. One common myth is that they are only for struggling businesses. In reality, many healthy, growing businesses use them proactively as part of sound financial planning. A line of credit is not a last resort, it's a working tool for managing timing gaps, smoothing out cycles, and staying ready for the unexpected.

Another misconception is that once you’re approved, the funds are yours indefinitely. Most credit lines are revolving, but they are still subject to periodic reviews. Lenders can reduce or freeze your limit if your financial profile changes or if the line goes unused for too long. That makes it important to treat a credit line as an active relationship, not a one-time setup.

A business loan provides a fixed amount of funding disbursed upfront, with repayment scheduled over a set term. The repayment amount is fixed and predictable, making it easier to plan around.

This structure supports larger investments where the full amount is needed at once.

With fixed payments and longer terms, business loans offer a sense of structure and discipline. They work best when the capital is fueling a defined project with measurable returns. When your business is in growth mode and ready to scale, a term loan can help make that leap possible.

The main distinction is control. A line of credit gives you access without obligation, while a loan delivers funding with a clear repayment timeline. Both can be useful, but only when matched to the right purpose.

Chasing the lowest rate without thinking through the financing structure often leads to problems. A line of credit may come with a slightly higher rate, but if you’re only using a small portion of it occasionally, the overall cost could still be lower than a term loan. On the flip side, relying on a line of credit to finance a major one-time project could become far more expensive than expected.

Imagine you’re running a retail business and you know Q4 sales will spike, but right now you’re tight on cash. You only need $15,000 to order extra inventory ahead of time, but you’re not sure exactly when you’ll need to pay your suppliers. A line of credit gives you the flexibility to draw that amount when the invoice hits. Nothing more, nothing less. Even if the interest rate is 2% higher than a term loan, you’re only paying interest on the funds you actually use, for the duration you use them. The total interest cost might be just a few hundred dollars.

Say you’re opening a second location. You’ve got contractors, equipment purchases, staffing, and a six-month runway before it turns profitable. If you try to fund that entirely through a line of credit, you could run into trouble. You’d be drawing down a large balance quickly, likely maxing out the credit limit, and making irregular payments without a clear payoff schedule. In that case, a structured loan with predictable payments and a clear end date keeps you disciplined and fully funded from day one.

It’s not about which one is cheaper on paper. It’s about which one fits the way your business operates. Smart financing isn't just about cost. It’s about context and control.

Start by clarifying the reason you’re looking for funding. Are you preparing for an ongoing need or solving a short-term issue? Do you need capital once, or repeatedly over time? Can you comfortably handle fixed repayment, or do you need flexibility?

If your revenue fluctuates or your expenses are unpredictable, a line of credit gives you breathing room. If you’re funding a specific growth initiative with a clear budget and timeline, a business loan can offer the stability you need to move forward with confidence.

The better you define the problem, the easier it is to choose the right solution.

You wouldn’t use a sledgehammer to hang a picture, and you wouldn’t rely on a pocketknife to build an addition. Financing works the same way. Matching the structure to the job reduces risk, avoids waste, and helps you stay focused on execution rather than course correction.

Good financing supports how your business actually runs, not how it looks on paper. The more realistic you are about your timing, revenue cycles, and goals, the easier it is to choose the option that won’t just fund your business, but work with it.

Ask yourself whether your current revenue can support fixed monthly payments without disrupting operations. You should also have a clear, trackable plan for how the funds will generate a return - whether that’s more customers, new contracts, or improved efficiency. If the loan would stretch your cash flow too thin or you’re uncertain about how it will drive growth, it may be worth revisiting your numbers or considering a smaller line of credit first. You can learn more about common mistakes to avoid when running a business here.

Yes, and many businesses do. For example, you might take out a loan to open a second location while keeping a line of credit open to handle day-to-day cash flow needs. The key is knowing the role each tool plays so you're not overlapping or relying on short-term credit vs. long-term loans for longer-term investments.

Nothing negative unless the account sits idle too long. Some lenders may lower your limit or close the account if there’s no activity for an extended period. Even if you don’t need the funds, it’s wise to draw and repay small amounts periodically to show usage and maintain access.

It depends on the lender, but lines of credit often require a stronger short-term financial profile since they’re designed for ongoing use. Lenders may look more closely at cash flow, bank statements, and recent business activity. Many newer lenders now offer streamlined options for both products, even for businesses without perfect credit.

In most cases, yes. The best time to get approved is when your business is financially healthy. Waiting until you’re in a cash crunch can limit your options or result in higher rates. Having a line of credit in place gives you peace of mind, even if you don’t need to use it right away.

It depends on the type of financing you’re applying for. For short-term business loans or lines of credit, most lenders look for a personal FICO score of at least 500. If you're applying for a longer-term business loan with lower rates and extended repayment, you'll typically need a score of 700 or higher.

Still, credit score isn’t everything. Lenders also look at cash flow, time in business, revenue trends, and how you plan to use the funds. If your score is on the lower side but your business is performing well, you may still qualify, just with different terms.

The more consistent your financials and the clearer your funding strategy, the better your chances of getting approved with terms that actually work for your business.

Every business needs capital. The difference lies in how and when you access it. A line of credit keeps you nimble. A business loan helps you commit to a longer-term plan.

Before comparing lenders, focus on what the capital is meant to accomplish. Once you're clear on the purpose, structure follows. And with the right structure, the financing works for your business, not against it.

If you’re nodding yes to these, a business line of credit may give you the flexibility you need without over-committing.

If that sounds like your situation, a business loan may be the better fit.

Every business runs a little differently. That’s why it matters to work with a team that listens first, then helps you figure out what kind of funding actually makes sense. Whether you’re considering a flexible line of credit or something more structured for long-term growth, we’ll walk you through the options and help you make a smart, confident decision.

Need fast access to capital? Apply now or call 877-400-0297 to speak with a funding specialist today.

Sign up for our newsletter to get exclusive updates and offers

Start our simple online application now.

See what our clients have to say about their experience with us.

![]()

© 2025 BusinessCapital, LLC

![]()